No fall in interest rates despite inflation hitting 2% target, Bank of England announces

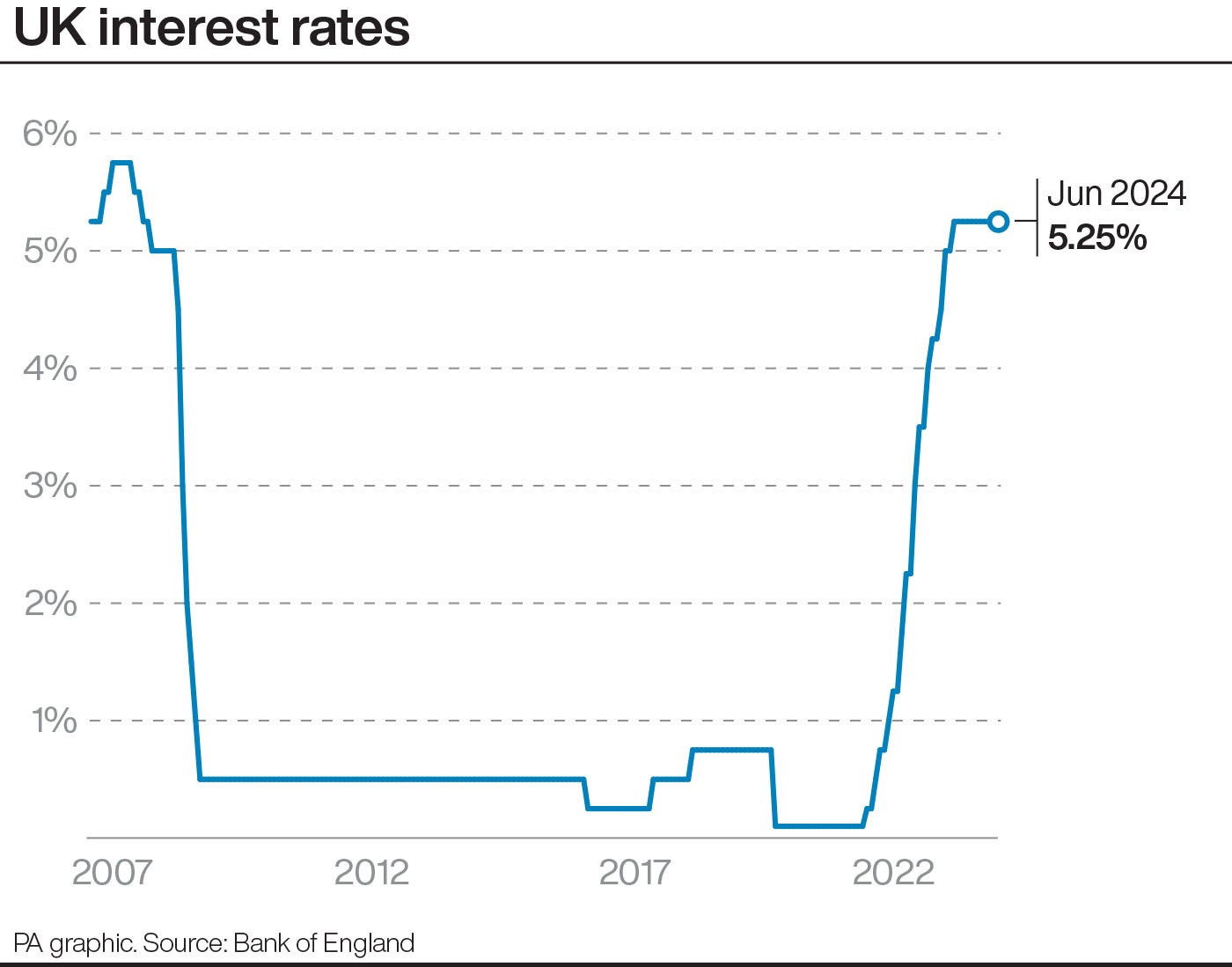

No relief for borrowers as Bank of England base rate to remain at 5.25 per cent at least until August

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

Your support makes all the difference.The Bank of England has declined to cut interest rates from their 16-year high – despite inflation finally falling to meet its target of 2 per cent.

Homeowners struggling with soaring mortgages will be forced to wait at least another two months for borrowing costs to fall, after the Bank’s nine-member Monetary Policy Committee opted on Thursday to hold the base rate at 5.25 per cent for the seventh consecutive month.

Bank of England governor Andrew Bailey had opened the door early last month to a rate cut, saying he was “optimistic that things are moving in the right direction” and that a June rate cut was an option – although by no means a certainty.

But despite data on Wednesday showing headline inflation fell from a recent 40-year high of 11 per cent to meet the bank’s target for the first time since July 2021 – reaching its goal quicker than the United States or euro zone – the medium-term picture is now less reassuring.

Services price inflation has fallen less than the Bank expected at the time of the last meeting – only declining to 5.7 rather than 5.3 per cent – and private-sector wage growth is almost twice the rate the Bank judges as compatible with 2 per cent inflation.

Interest rates will remain at 5.25 per cent at least until the Monetary Policy Committee’s next meeting in August. Seven members of the committee voted against a 0.25 per cent cut on Thursday, while two – Dave Ramsden and Swati Dhingra – voted in favour.

The Bank’s governor, Andrew Bailey, said policymakers “need to be sure that inflation will stay low and that’s why we’ve decided to hold rates at 5.25 per cent for now”.

However, financial markets have reduced bets of a rate cut happening in August either. On Wednesday, they priced in only a 30 per cent chance, with a first move more likely in September and a risk of a delay until November, similar to expectations for the US Federal Reserve.

Homeowners have been badly hit by the sudden rise in interest rates. Some 1.6 million mortgage-holders will come to the end of their fixed-rate deals this year, and will face an average hike of about £1,800 annually on their repayments, the Resolution Foundation previously estimated.

The latest Bank of England figures suggest the value of outstanding mortgage balances with arrears has risen 50 per cent since 2022 to bring the total to more than £21bn.

And analysts at investment firm Hargreaves Lansdown calculated last month that the mortgage repayments of 2.1 million homeowners – one in four – will exceed 25 per cent of their disposable income by the end of this year, putting them at risk of arrears.

But the Monetary Policy Committee warned on Thursday that it “will need to remain restrictive for sufficiently long to return inflation to the 2 per cent target sustainably in the medium term”, warning of a risk that inflation – which is set to rise again later this year – could become “embedded” above 2 per cent.

The committee will “continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation”, it said.

The pound edged lower against the US dollar and the euro following the Bank’s decision not to cut rates, slipping 0.2 and 0.1 per cent respectively.

Federation of Small Businesses chair Martin McTague said the decision was widely predicted but “no less disappointing for it”, warning that “the high plateau rates are currently stuck at is now undermining growth as small firms struggle to access affordable finance to help them expand”.

While the UK slipped into a recession in late 2023, the economy grew 0.6 per cent in the first three months of this year. The Bank said on Thursday it expects GDP growth of 0.5 per cent in the second quarter of 2024, an upgrade from its 0.2 per cent forecast in May.

But union chief Sharon Graham, of Unite, said: “Once again, the Bank of England has failed to act in the interest of workers and hard-pressed families. Major economies across the world have cut interest rates and the UK must follow suit.

“High interest rates boost the profits of city bankers but hit all of us paying mortgages and rents in the pocket. It’s time for the bank to get a grip.”

And Dr George Dibb, of the IPPR think-tank, warned the Bank has “tightened the screws too much for too long, holding back the UK’s economic recovery”, adding: “The Bank has to balance lingering price rises, notably in services, with the UK’s zero economic growth and a cooling labour market.

“With inflation expectations back down to pre-pandemic levels, it’s time for the Bank to switch gears, support the economy more, and cut rates.”

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments