Trump effect: UK borrowing costs hit highest level since Brexit vote

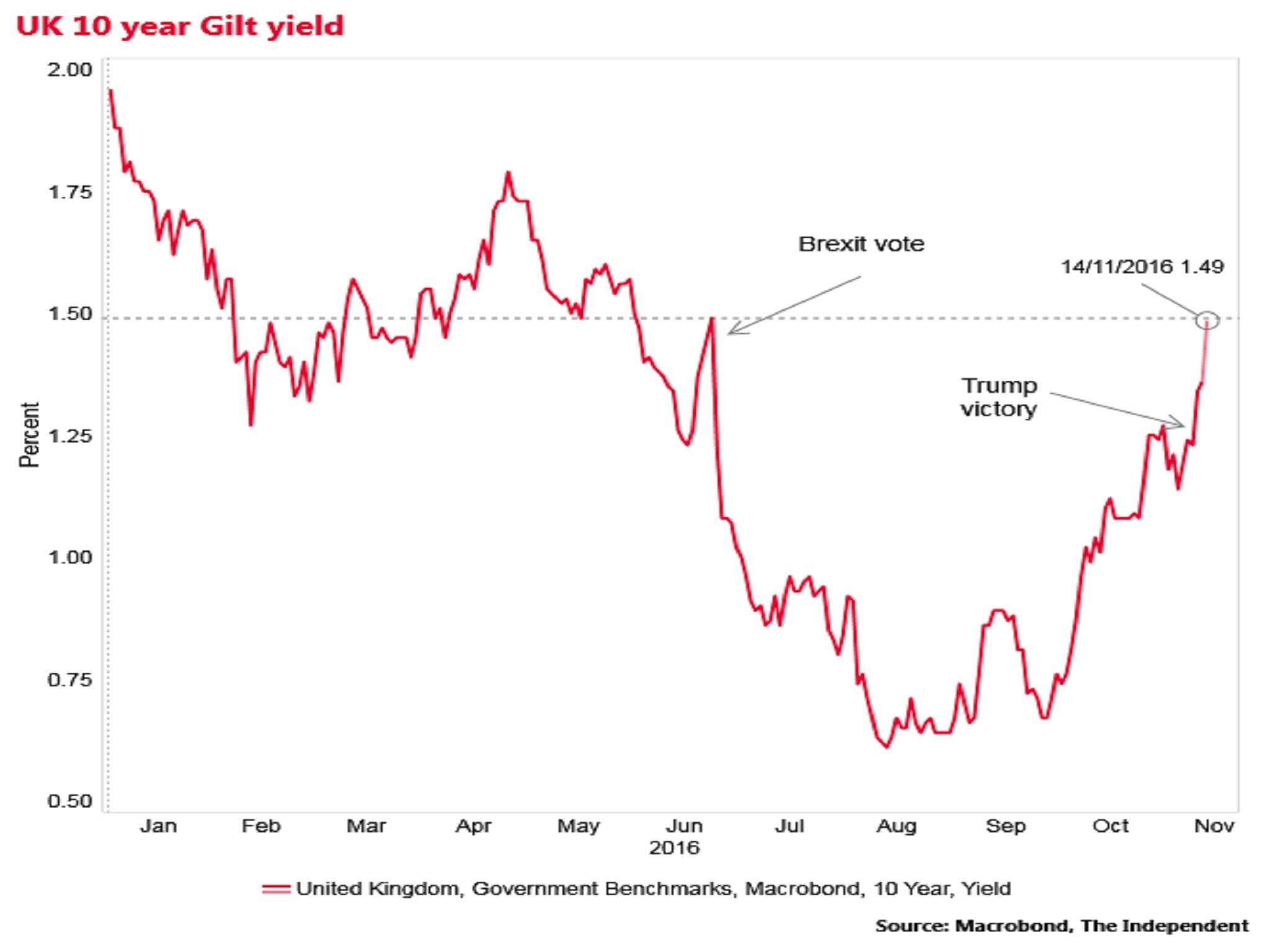

10-year gilt yields have spiked to 1.49 per cent, the highest since the end of May – and almost 1 percentage point higher than three months ago

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

Your support makes all the difference.The UK’s 10-year borrowing costs have now risen above the level at the time of the Brexit vote – increasing the cost to the Government of funding the national debt and with City of London analysts pointing to the spillover affect of Donald Trump's presidential election victory in the US.

Ten-year gilt yields – the effective benchmark interest rate the Government has to pay to borrow from the capital markets – plummeted after the June referendum, falling from 1.383 per cent to a new historic low of 0.506 per cent in August.

This was seen as a consequence of a flight to the safety of UK government debt by nervous investors and also an indication of expectations of much looser UK monetary policy.

But gilt yields, which move in the opposite direction to gilt prices, have been steadily climbing since then, reaching 1.380 at the end of last week.

And today they have spiked to 1.49 per cent, the highest since the end of May – almost 1 percentage point higher than three months ago.

UK borrowing costs rising...

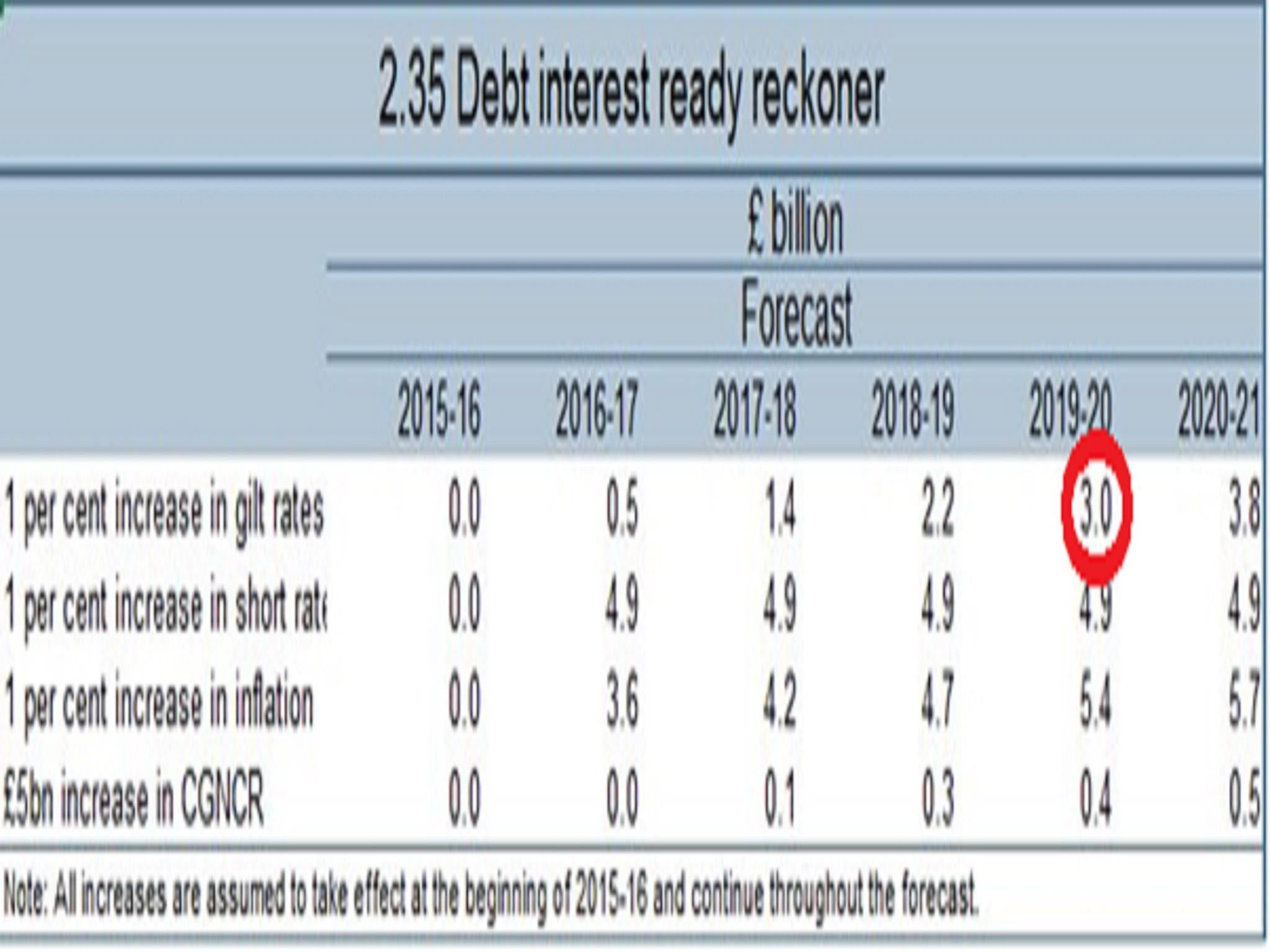

This will automatically have a negative impact on the public finances.

In March the Office for Budget Responsibility estimated that each 1 percentage point increase in Gilt yields adds another £3bn to the deficit by 2019-20.

...bad for the public finances...

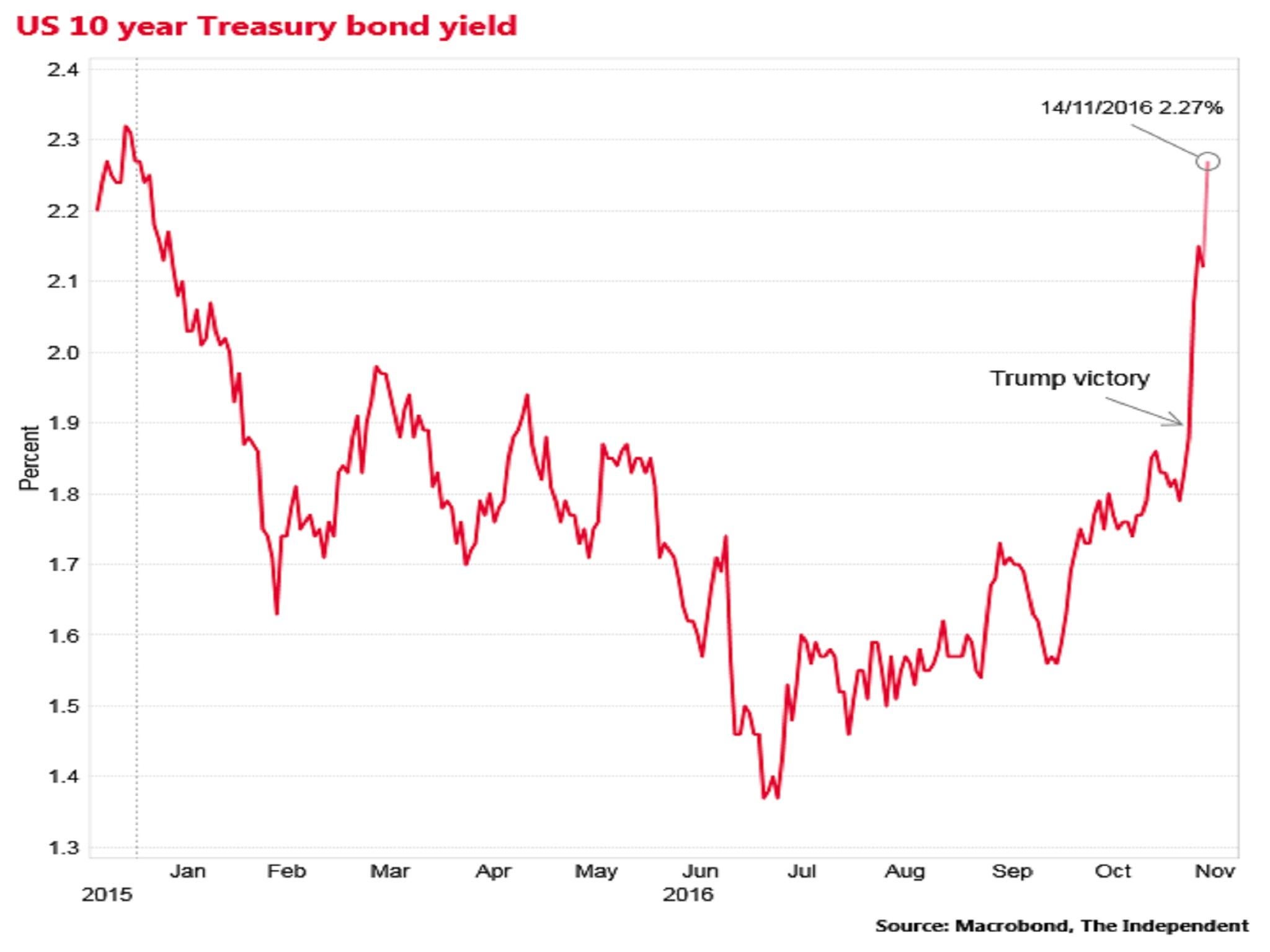

US government borrowing costs have also been rising in the wake of the election of Donald Trump, with 10-year Treasury yields spiking from 1.88 per cent last Wednesday to 2.276 per cent today.

...US borrowing costs rising too

Analysts say this spike is based on a market belief that Mr Trump will follow through on his plans for a major infrastructure investment push in the US – and possibly income tax cuts.

They argue that the sell-off of US Treasury bonds is dragging UK Gilt prices down in its wake, since the two are often considered to be rough substitutes by investors.

“UK gilts are reacting to the sell-off in US rates. In particular markets are focused on the scope for fiscal policy in the US to take a bigger role, and the potential for higher inflation,” said Mike Amey of the bond-specialists investment company Pimco.

Eurozone government bonds have also been hit by a major sell off since the US election last week, with around $1 trillion (£800bn) of value knocked off global bond prices according to Reuters.

But other analysts said the increase in UK gilt yields also reflected a belief in markets that the Bank of England will now put up short-term interest rates sooner than previously expected thanks to a coming jump in inflation flowing from the sharp fall in the pound since the Brexit vote and also reasonably robust UK GDP growth despite the Brexit vote shock.

“We think that markets have got it broadly right,” said Capital Economics.

“We expect the [UK] economy will perform reasonably well over the next few years and by 2019, or possibly even sooner, a move away from the current ‘emergency’ levels of interest rates will be justified.”

The Chancellor, Philip Hammond, has signalled that he will implement his own state infrastructure boost for the UK in the 23 November Autumn Statement which is also likely to push up gilt yields, although analysts expect this stimulus to be quite limited in size.

By historic standards UK and US bond prices are still exceptionally low, meaning that the Government can borrow for less than nothing once allowance is made for expected inflation.

Before the 2008 financial crisis UK 10 year gilt yields were around 4.5 per cent and Treasury yields were were around 4 per cent in the US.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments