Hamish McRae: The Brics and the developed economies are all rebalancing. Over the next year the latter will probably come out on top

Economic View: The gap has narrowed between emerging markets and the US, UK, Japan and eurozone

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

Your support makes all the difference.The great rebalancing act continues – rebalancing, that is, of growth between the G7 and the Brics. The past few days have seen a series of news stories in both the emerging and developed worlds that highlight the shift. The questions now concern how far this rebalancing might go and the consequences of that.

To start with the Brics, two of them look like heading into recession this year. Russia was poised on the brink of recession even ahead of the events in Crimea. Now it looks pretty certain to show negative growth for at least a couple of quarters. The only thing that might change this being a surge in oil and gas prices, for energy is such a large part of the Russian economy that a rise in the price would automatically increase the size of the country's GDP.

Receiving much less attention has been the slowdown in Brazil. The current data is not too bad, for there was some growth in the final quarter of last year after a dip in the autumn. Market forecasts are for growth of 1.5 to 1.9 per cent this year. But the past few days have seen new concerns about the combination of slow growth and high inflation, stagflation. Brazil's credit rating was downgraded by Standard & Poor's this week, citing the poor fiscal outlook and deteriorating growth. It is hard to see quite how the country will escape from this and it is quite possible that the economy will dip into recession later this year or early next. On a longer view Brazil has great growth prospects, unlike Russia, but in the short term it faces politically difficult reforms.

The other two Brics, China and India, face different issues. In the case of China it is how to maintain growth at around 7 per cent, somewhat slower than in recent years, and not let it dip further. In India it is how the new government, to be elected in a few weeks' time, can push up performance after a disappointing year. The basic point here, though, is that while both of these countries are growing solidly, the burst of optimism of three years ago has been replaced by a more measured attitude.

So there has been a reassessment. Taken as a whole, they and the rest of the emerging world will grow more swiftly than the developed world. There is no question about that. But the gap has narrowed.

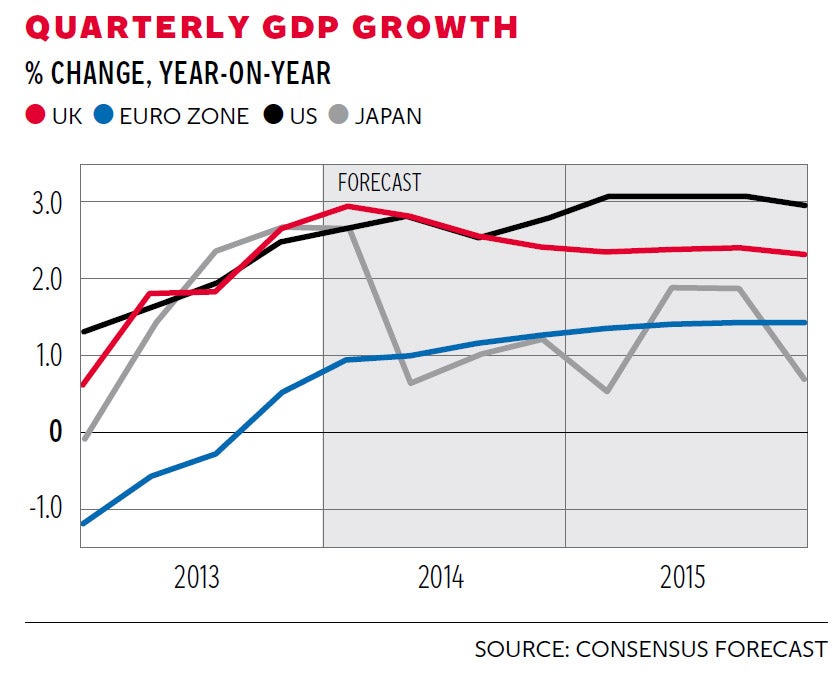

It has been narrowed by a stronger performance in the developed world too. The graph shows the consensus forecasts for this year and next for the US, UK, Japan and the eurozone. The obvious point here is that a year ago only the US was seeing reasonable growth, whereas for the next two years all three regions are expected to continue to grow, albeit in the case of Japan and the eurozone quite slowly.

In structural terms I don't think there has been much of a change. But in cyclical terms there can be no doubt that the cycle is favouring the developed world, with even the laggards being pulled along by the rest. There is only one country in the entire developed world that I can find that is not expected to grow this year, and that is Greece. Even Greece is expected to grow in 2015. But the flip side of this is that the Asia-Pacific region is expected to grow by 4.6 per cent this year, faster than any country in the developed world.

This distinction between the long-term structural balance in the world and the short-term cyclical forces is absolutely crucial to understanding what is going on. The first favours the Brics; the second the G7. So what should we look for next?

This reassessment, rebalancing, call it what you will, has some way to run. The drift of the news through this year and next will favour the developed world as the cyclical upswing strengthens. The parts of the developed world that are expanding fastest will experience higher interest rates first. You can have a debate about the timing of the first increase in UK interest rates – will it be this coming November or will we have to wait until next year? – but no one doubts that a rise is now firmly on the way. We all know this: that is why there has been a surge in homeowners fixing their mortgages.

At the other end of the scale, the eurozone may move in the other direction. There has been a lot of speculation in the past few days that some form of QE will be adopted in Europe, particularly if inflation dips further and certainly if it moves negative. There is not much point in adding to this, except to observe that if Europe faces deflation it is common sense for the European Central Bank to use unconventional methods to try to nudge prices upwards. That is its mandate. My guess is that further measures are now an odds-on bet, but we will see.

The US will tighten, of course. The tapering down of the monthly purchases of Treasury securities will continue and those purchases will cease in the autumn. The focus will then switch to the pace at which its interest rates will climb. While at the moment there is a lot of understandable attention paid to what its new chairman, Janet Yellen, says, the key determinant will be the performance of the US economy. The latest numbers, for example for consumer confidence and housing starts, have been pretty positive.

Numbers matter more than words. If the numbers surprise on the upside, as they are doing in the US and UK, and from a rather lower base also in Europe, then the "developed world good" mood will continue. If, on balance, the numbers from the Brics disappoint, the "emerging world bad" mood will also continue. But both moods exaggerate what is actually happening. Welcome the recovery in the developed world, but note the structural shift towards the emerging world runs on for a long while yet.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments