Millennial Money: Stop using paper checks, already

You’re probably not using paper checks for most things

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

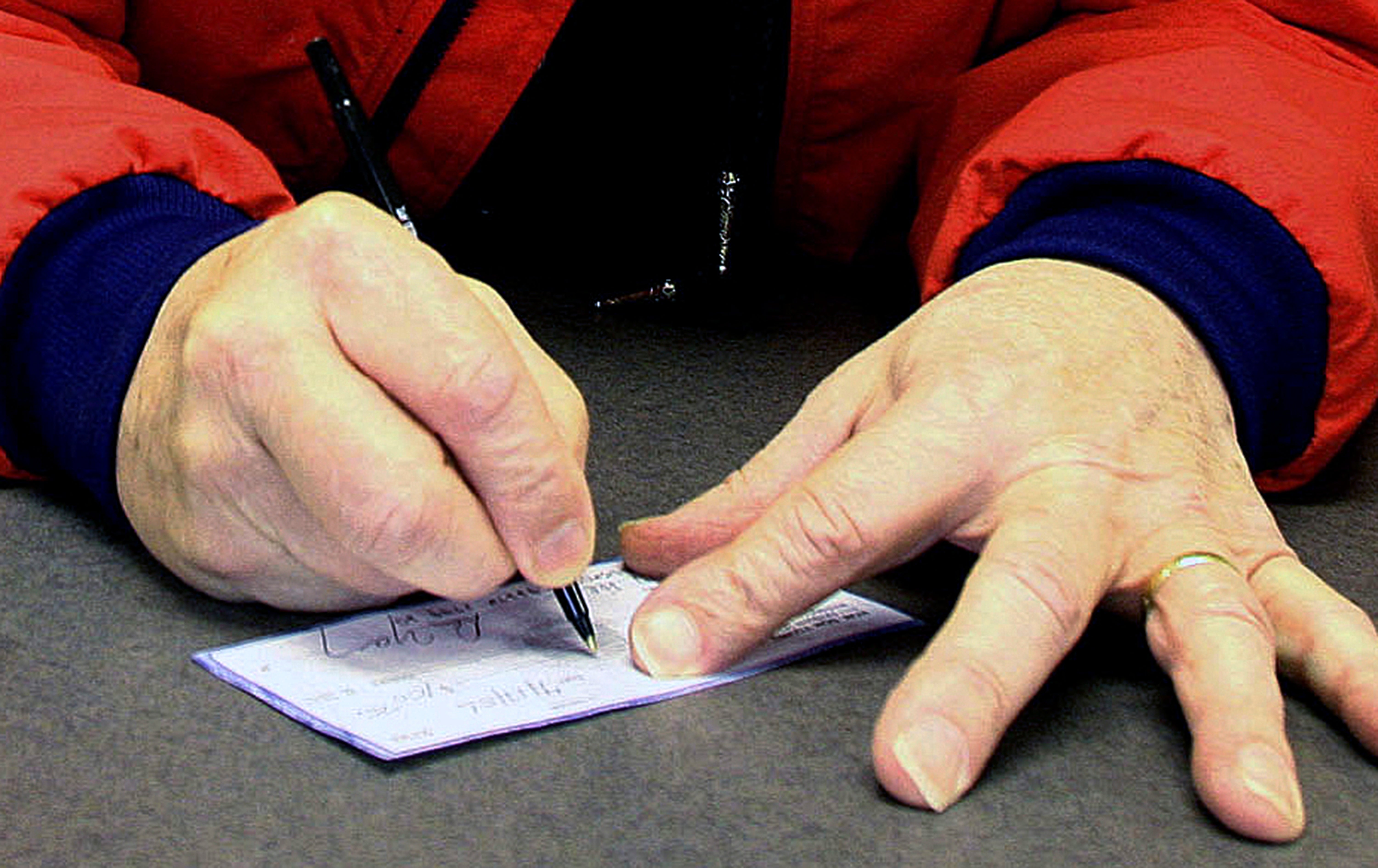

Your support makes all the difference.Sure, you’re probably not using paper checks for most things. But are you returning payments to medical providers and insurance companies in the mail? Paying by check for the random parking ticket or your child’s piano lessons? Now is a good time to stop: Check fraud tied to mail theft is up nationwide, according to a February alert from the Financial Crimes Enforcement Network. And letter carrier robberies are also on the rise.

This is partially due to the effects of the pandemic, when thieves targeted government relief checks in the mail. “Fraudsters just went back to tried-and-true potential attack factors that seemed to be working,” says Michael Bruemmer, head of global data breach resolution for Experian.

The U.S. Postal Service is vulnerable, and thieves who can access your checks can change the amount and ferret those funds right out of your bank account. And then it can take weeks to get the funds back.

“It’s absolutely a life disruption event when you mail a check and it’s been intercepted,” says Mary Ann Miller, fraud and cybercrime executive advisor and vice president of client experience at consumer identity company Prove. “That can take all the money out of your account at once.”

Here are some steps to keep yourself safe from check fraud — and what to do if you’re a victim.

USE PAYMENT ALTERNATIVES

Look for ways to pay your bills that don’t require using the mail. Check your statement for online payment instructions, for example. “We are beginning to see more online options,” Miller says. “In fact, some medical providers, like One Medical, have a very nice option to pay from a mobile app along with all of your medical information. I find it super helpful and modern.”

If you’re paying individuals, ask if they’ll accept electronic payment through PayPal, Venmo, Zelle or another cash app. “There’s really no need to be writing checks today,” Bruemmer says.

Working with a vendor that doesn’t offer an easy way to pay online? Call and ask if you can pay over the phone. “Paying by phone via the IVR — interactive voice response — or a live customer service representative is definitely a preferred option,” Miller says. “Just make sure you are calling the correct number for the utility or medical provider.”

And in general, experts recommend using credit cards to transact, whenever possible. “You have a lot more protection globally with a credit card, if you’re traveling internationally, or if you’re buying things online,” says Derek Miser, an investment adviser and CEO at Miser Wealth Partners in Knoxville, Tennessee.

SEND CHECKS SAFELY

If you must send a check, take steps to lower the chances of financial mayhem. If it’s a big payment, consider using a shipper like UPS or FedEx. “They do accept checks and provide a tracking number,” Miller says.

If you’re using the U.S. Postal Service, send your payment in a security envelope and take it directly to the post office, bypassing mailboxes and mail carriers. You can also write your checks using a black gel ink pen to make it harder for criminals to wash your checks (the ink soaks into the paper).

If you’re sending a check to someone, ask them to let you know once they receive it. That way, if too much time has passed and the recipient hasn’t gotten the check, you can place a stop payment, Miller suggests.

One last safeguard: Keep enough funds in your checking account to pay the bills, but put the rest elsewhere, such as a linked savings account. The smaller your checking account balance, the less money that can be accessed by someone forging a check against your account.

TAKE ACTION IF A CHECK GOES AWRY

If you suspect a check has fallen into the wrong hands, call your bank right away. Then file a police report and contact the person or business that was meant to receive the check. If you were making a payment, you may have to make arrangements to make another payment to prevent late fees or interest.

Be forewarned: Processes for returning fraudulently lost money to bank accounts vary by institution, and some timelines are lengthy. “The customer generally is made whole, but that could be months,” Miller says.

In the meantime, consider putting a fraud alert on your credit reports in case someone tries to open credit in your name, and go over your bank statements and credit reports with an eagle eye. Note that you’re eligible for a free credit report from each of the three major reporting agencies each year at AnnualCreditReport.com.

You can also set up check monitoring at some banks, from which you’ll receive text messages or alerts when transactions over a certain amount are cashed.

“I would say now that just about every bank has some sort of monitoring,” Bruemmer says. “Take advantage of that free alerting that comes from being a member of a financial institution.”

_______________________________

This column was provided to The Associated Press by the personal finance website NerdWallet. Kate Ashford is a writer at NerdWallet. Email: kashford@nerdwallet.com. Twitter: @kateashford.

RELATED LINKS:

NerdWallet: How to write a check: Fill out a check in 6 simple steps https://bit.ly/nerdwallet-how-to-write-a-check

Annual Credit Report.com https://www.annualcreditreport.com/