Bank of England Governor gets his forward guidance on interest rates wrong

Earlier this year Mark Carney signposted a rate rise from the Bank of England relatively soon. But a deterioration of the global economy seems to have pushed it out once again

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

Your support makes all the difference.In July Mark Carney gave a speech beneath the vaulted ceiling of Lincoln Cathedral in which the Bank of England Governor said that, in his view, the decision about whether the Bank should start lifting interest rates from their historic lows of 0.5 per cent would probably “come into sharper relief around the turn of this year”.

And so it has. But not in the manner most people imagined. Instead, the latest Inflation Report from the Bank of England, published on Thursday, is so pessimistic about the negative impact of the global slowdown on the UK economy that it effectively takes a first rate rise off the table until deep into 2016 or even 2017.

What has come into sharper relief is not a rate rise but the fact that the cost of borrowing is unlikely to go up any time soon – at least not if the world economy pans out in the way the Bank currently expects.

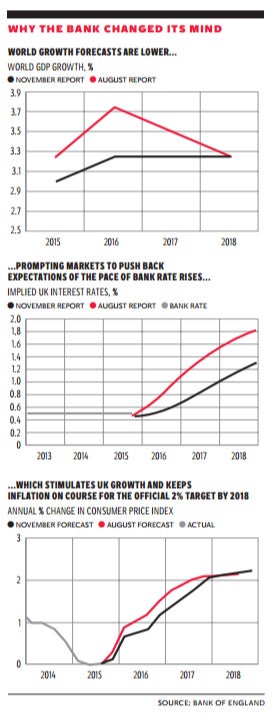

The Bank of England thinks the economic and financial outlook has changed rather radically since its last quarterly Inflation Report in August. The figures in the latest report show global growth will be slower than it had expected, mainly because of a weaker outlook for big emerging-market economies such as China.

The Bank expects global growth this year to come in at 3 per cent, down from the 3.25 per cent expected three months ago. Growth is also seen half a per cent lower in 2016 and quarter of a percent lower in 2017. According to the Bank this slowdown will have an impact on UK economic GDP growth, primarily in the form of lower demand for exports.

The Bank also thinks a weaker global economy will mean lower global commodity prices, which will help depress UK inflation, which was at minus 0.1 per cent in September, well below the Bank of England’s official target of 2 per cent.

Yet the Bank also identifies a large offsetting economic effect in its latest report. It notes that financial markets’ expectations of the rate of future interest rate increases by the Bank have also altered significantly since August. The expected pace of monetary tightening is now much less severe. It is clear from the Bank’s figures that this “flattening of the yield curve”, by keeping down the cost of borrowing for longer, helps to stimulate the UK economy. It lifts both GDP and inflation relative to what would otherwise have happened.

The happy outcome is that the Bank’s growth and inflation forecasts haven’t actually shifted very much since August, despite the intensification of the global economic headwinds.

Inflation is forecast to be somewhat weaker next year, hitting just 1.1 per cent at the end of 2016, down from 1.5 per cent in August. Yet by end of 2018 the lost ground has been made up, with consumer price inflation back up to the 2 per cent target – as was forecast in August.

“The lower path for Bank Rate implied by market yields would provide more than adequate support to domestic demand to bring inflation to target even in the face of global weakness,” Mr Carney explained.

The Bank of England’s rate-setting Monetary Policy Committee voted by eight members to one to keep rates on hold at 0.5 per cent. The only dissenter, once again, was the external member Ian McCafferty, defying the expectations of many City of London analysts that he would win support for his calls for a 0.25 percentage point increase.

The surprise was reflected in the currency markets, with sterling instantly falling by more than a cent against the dollar to $1.53. It also dropped more than a cent against the euro to hit €1.40.

The yield curve figures used by the Bank of England in its Inflation Report related to the 15-day average up to 28 October. The curve has steepened slightly since then and markets are now pricing in the first interest rate rise in December 2016. Yet the overall message from the Bank is nevertheless clear: rates can remain lower for longer without triggering excessive inflation next year.

Andrew Goodwin of Oxford Economics described the Inflation Report and the minutes from the latest meeting of the Monetary Policy Committee as “indisputably doveish” and pushed out his estimate of the first rate hike from May 2016 to November 2016. Oliver Harvey at Deutsche Bank said near-term interest rate hikes by the Bank were now “off the table” and said Threadneedle Street had “explicitly validated” the big shift in market expectations since the summer of the timing of the next rise.

Some analysts warned of the economic dangers of keeping rates low for even longer. James Sproule, chief economist at the Institute of Directors, cited “genuine apprehension over asset prices, the misallocation of capital and consumer debt”. Halifax reported that house prices increased by 9.7 per cent year on year in October, up from 8.6 per cent in September.

At a press conference Mr Carney said he was “conscious” of moves in house prices but he also stressed that mortgage underwriting standards were much improved.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments